Summary

· I bought shares in Odyssey Gold (ASX:ODY) during the past few weeks. I will continue buying shares.

· I was not planning a report on them, but they now make 5% of my portfolio. So, I am writing this report in the spirit of transparency. Bear in mind its market cap is A$50 million, so expect little liquidity.

· On this report I argue that Odyssey is in a unique sweet spot: Developer fully funded to potential production within the next 12 months.

· I argue that Odyssey is the cheapest gold stock in the ASX within this sweet spot.

· Chances of a takeover are high thanks to the low capex (A$5M) and its near term production profile.

· The two keys: Odyssey is cheap and has a tailwind.

o Cheap: Relative to other gold stocks on the same stage and size.

o Tailwind: Gold production in 2026 or 2027 thanks to a potential toll mining agreement.

· The current framework is a non-binding MOU with Monument Mining for potential toll processing at Burnakura (with over 10 Mt of additional regional mill capacity nearby), this positions Odyssey for a low-capex path to production in 2026–2027.

· If the toll mining agreement does not work out, Odyssey will not reach production near term. However, you would still hold one of the cheapest gold developers in terms of EV/oz ratios.

Alberto’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Introduction: History of the company

I love studying world history, and this often comes handy when analysing stocks. I always look at the story behind each company before making a purchase.

Odyssey Gold is an Australian gold development company focused on projects in Western Australia, particularly in the Murchison Goldfields region. Western Australia is by far the best region worldwide in terms of geology, infrastructure, human capital and permitting.

The company was incorporated in 2005, originally under the name Odyssey Energy. For its first 15 years, it operated under that name, though specific details on its early activities are not detailed in public profiles. It appears to have been a listed exploration entity with limited or evolving focus prior to its pivot.

The key turning point in its history came in 2020, when the company shifted its strategy toward gold exploration in Western Australia. In late 2020 (around October), it entered into agreements to acquire interests in high grade gold projects in the Murchison region. Notably, it acquired an 80% interest in the Stakewell Gold Project.

Shortly after, on October 22nd, 2020, it announced the acquisition of the Tuckanarra Gold Project (also targeting 80% interest) from Monument Mining (a TSX listed company), consolidating adjacent tenements covering historical goldfields in the area between Meekatharra and Mount Magnet.

These acquisitions gave it a combined land position: Around 176 km² across the projects, with 80-100% interests. Furthermore, this is in a prospective gold district that has hosted significant historical production and sits in a region with over 35 million ounces of gold endowment.

To reflect this strategic refocus on gold, the company changed its name from Odyssey Energy to Odyssey Gold in November 2020. Although on some websites like investing.com the stock remains named Odyssey Energy.

Since then, Odyssey Gold has focused on exploration and development of these gold assets (primarily the Tuckanarra and Stakewell projects), aiming to advance toward potential mining.

The company has continued activities such as drilling, resource reviews, and fundraising (e.g., placements and securities issuances in subsequent years). But its core history revolves around the 2020 rebranding and acquisition driven pivot to become a dedicated gold explorer in Western Australia’s prolific gold belts.

The key pivotal moment since 2020 came in the past year when Odyssey reached a potential toll mining agreement. Enabling them to achieve production with very low capex, albeit sharing in the profits.

What is a toll mining agreement?

A toll mining agreement is a contractual arrangement in the mining industry where one party (typically the owner of ore or mineral material) delivers their raw ore to a third-party processing facility (such as a mill, concentrator, or smelter) for treatment or processing.

The facility owner charges a fixed fee (the “toll” or tolling fee) per ton of ore processed or based on agreed terms, and the processed product (e.g., gold doré, concentrate, or refined metal) is returned to the ore owner or accounted for accordingly.

These agreements offer several advantages, particularly for smaller or developing mining operations:

Lower capital expenditure: The ore owner avoids the massive cost (often hundreds of millions of dollars) of building, permitting, and maintaining their own processing plant. This is especially valuable for junior explorers or companies with smaller scale deposits that cannot justify standalone infrastructure.

Faster path to production and cash flow: Operations can start generating revenue sooner by utilizing existing, permitted, and operational third-party facilities rather than waiting years to construct a new mill.

Access to expertise and proven technology: The toll processor typically has experienced operators, optimized circuits, and economies of scale. This leads to potentially higher recovery rates and efficiency than a new or small-scale plant could achieve initially.

Reduced operational risk and complexity: The ore owner focuses on mining/exploration while outsourcing processing. This often includes handling environmental compliance, tailings management, and regulatory requirements at the plant.

Flexibility and scalability: Agreements can cover specific tonnages (e.g., 100,000–500,000 tonnes over a set period), with options to extend or adjust volumes. This allows producers to ramp up/down based on mine output or market conditions.

Potential cost predictability: Fixed or formula-based toll rates provide more predictable processing costs compared to building and running a plant (though rates may include escalators for energy, labour, or inflation).

Byproduct or additional revenue opportunities: In some cases (e.g., polymetallic ores), the processor can handle complex recoveries, and the ore owner benefits without investing in specialized equipment.

While beneficial in many scenarios, toll agreements are not always ideal:

Toll fees can be significant and eat into margins (especially if recoveries are lower than expected or metal prices drop).

Dependence on the processor’s availability, performance, and reliability (delays, downtime, or disputes can impact cash flow).

Less control over processing parameters, scheduling, or optimization compared to owning the facility.

Transport costs (hauling ore to the distant mill) add expense.

Therefore, Odyssey is facing higher costs than the average gold miner. But with the exceptionally low capex and the current gold price, I argue this is the ideal way to play the current stage of the bull market in precious metals.

The thesis and valuation

The thesis is simple. While other mining stocks have to spend hundreds of millions of dollars just to make a small gold mining operation possible, Odyssey may be able to achieve this with A$5M capex and a toll mining agreement.

Other ASX listed stocks like Auric Mining, Lefroy Exploration, Challenger Gold, Western Gold Resources or New Murchison Gold have all executed this same strategy successfully. This has pushed their share price between 200% and 900% in the past 18 months alone.

Therefore, low capex plus sharing in through the profits in a toll mining agreement is a proven strategy. Odyssey is not trying to reinvent the wheel, which is good.

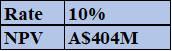

FCF for the project. 100% attributable.

The table above is mostly in tons, which may be confusing for most mining investors as troy ounces are the most common measurement in precious metals. The reason I used tons is because the costs of the toll mining agreement are measured in A$/t. Bear in mind the table is measured using 100% attributable figures, while ODY owns 80% of the project.

NPV for the percentage of the project Odyssey owns would be A$404M versus a market cap of A$42M today. Even if we include all the OTM options, the fully diluted market cap would be A$53M.

NPV for the project. 80% attributable. At A$7000/oz.

Yes, this NPV and cash flows assume a gold price of $5000/oz (or A$7000/oz), which is optimistic. But according to my estimates, breakeven is near $2625/oz, so we would need a 51% drop in gold prices for the project not to make sense. This 51% drop is possible, albeit unlikely. And considering the massive discount the company is trading at versus NPV, I would say the margin of safety is significant.

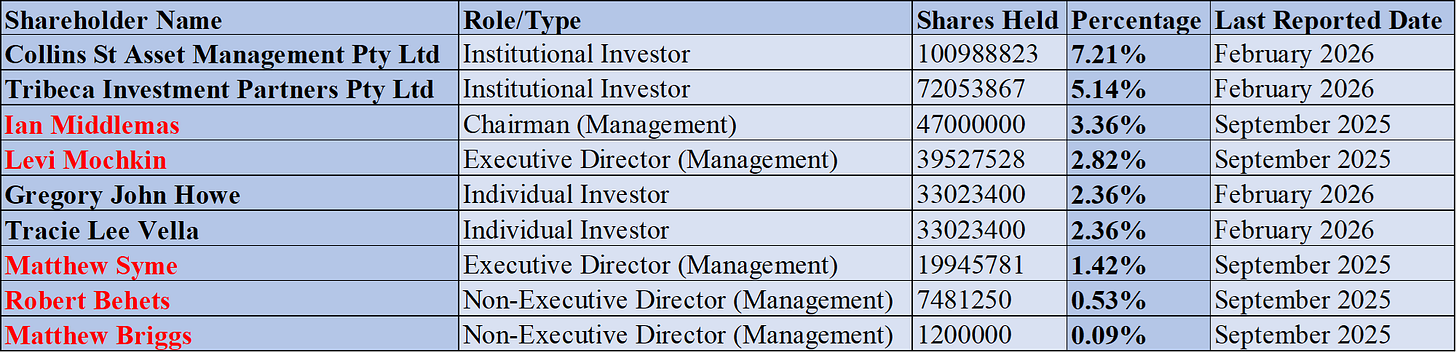

Ownership of Odyssey Gold. Management names in red. Own research.

Management owns 8.22% of the stock. Collins St is the largest shareholder which is great since they are one of the most sophisticated resource investors in Australia.

Most importantly, management bought some of their stock through participation in share placements, where they paid cash consideration for the shares. While some performance rights have been granted, I argue it is critically important that directors have put some of their own money into the stock.

Comparison versus peers

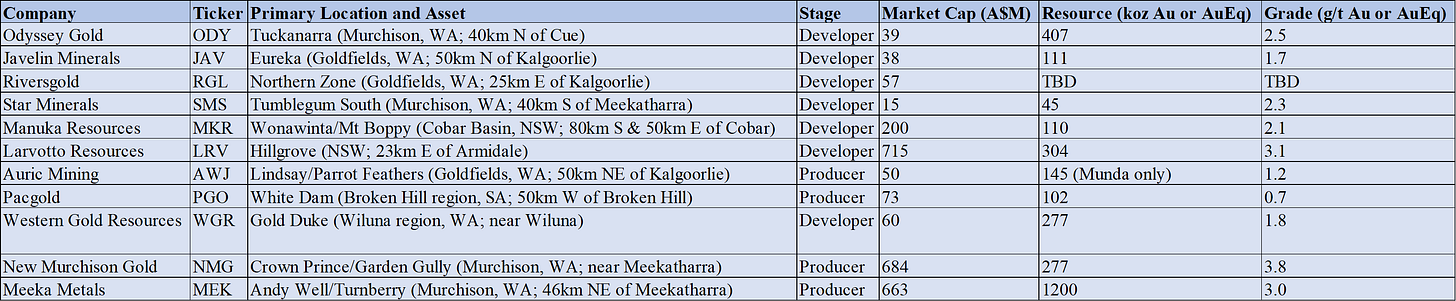

Comparison table among peers. Own research.

ODY trades at one of the lowest EV/oz ratios (A$86/oz) among peers, signalling significant undervaluation relative to its 407koz resource at 2.5 g/t. As a developer with a scoping study due soon and toll milling partnerships (e.g., Burnakura access), it is poised for a re-rating as it advances toward 2026-27 potential production (30-50koz pa est.).

If the toll milling partnerships work, I expect ODY to be in production towards the second half of 2026. If the current toll mining agreement does not work out, production could well be delayed to 2027. But an agreement with Gylden Resources is also possible and therefore the current toll agreement is not the only viable option.

There is also the possible scenario that no toll milling partnerships work out, I pointed this out on the summary. But even then, as I said earlier: “you would still hold one of the cheapest gold developers in terms of EV/oz ratios.”.

There are other gold developers that are as cheap as Odyssey in terms of EV/oz ratio. An example is Radius Gold, but Radius does not have a clear path towards near-term production.

Regarding the peers:

Javelin Resources has 261 million shares outstanding and 129 million stock options. Therefore, the price ceiling on the stock is a hurdle. And the dilution will be significant. Its smaller resource (111koz) limits scale/upside compared to Odyssey.

Riversgold lacks a JORC resource but offers massive upside from its shallow oxide project, with an 800% land expansion announced in 2026, boosting scale via partnerships.

It offers pure exploration torque. Risks: High (no resource = uncertainty), but recent drilling assays pending could become catalysts. I argue it does not offer any margin of safety though.

Star Minerals only has a 45koz resource at 2.3 g/t and a very modest production target (10-15koz pa est.), limiting its re rating potential and cash flow generation compared to ODY’s projected 30-50koz pa.

Manuka Resources has A$24M in debt and A$8 in cash. I generally view it as inferior to ODY for pure gold exposure and valuation upside: Its resource is diversified (primarily silver with gold credits, lower gold only ounces 110koz Au equiv.).

It is located in NSW, meaning higher jurisdictional/permitting risks and less gold infrastructure synergies than WA. It trades at a much higher EV/oz with a larger market cap that already prices in significant optimism, limiting re rating torque compared to ODY’s compact.

Larvotto in my opinion has gone into an absurd valuation because of antimony. This niche metal has gathered a lot of attention from investors and turned into a bit of market euphoria. I much rather stay away from metals in which investors are too optimistic. Furthermore, management only owns 3% of the stock.

Auric Mining is about to restart the Parrot Feathers open pit gold deposit within the Lindsay’s Gold Project (located 50km northeast of Kalgoorlie, WA). There is no published JORC compliant Mineral Resource Estimate (MRE) for Parrot Feathers. Website looks great, so I respect management for that considering the low market cap. However, it offers little to no margin of safety that I can see.

Pacgold has 431 million shares outstanding and 103.7 million options in the money. They own the White Dam project. GBM resources, the previous owner of White Dam, faced typical challenges in the sector: Variable recovery rates, copper content complicating processing. GBM had plans for a SART plant to address copper issues before the sale. These problems are common in many heap leach gold operations.

A SART plant is a specialized processing facility used in gold mining operations, particularly those involving cyanide leaching of ores that contain significant amounts of cyanide soluble copper (and sometimes other metals like zinc or silver). SART stands for Sulfidization, Acidification, Recycling, and Thickening.

Pacgold is not planning a SART plant, so they may encounter the same problem GBM did: Soluble copper consumed excess cyanide, raising reagent costs and potentially lowering gold recovery/efficiency (a classic heap leach polymetallic problem). Therefore, I am not willing to invest in it.

Western Gold Resources looks a lot better than Pacgold. With a fresh 277koz resource at 1.8 g/t and Decision to Mine approved, WGR is on track for first gold in late Q1 2026 via toll milling at Wiluna.

Its EV/oz (A$202/oz) is attractive for a funded, de risked developer, with Stage 1 targeting 42.8koz over 14 months (15-25koz pa est.). This could drive a producer re rating. However, given the lower (than ODY) grade at Western Gold and their smaller resource, I prefer Odyssey.

New Murchison Gold and Meeka are already in production. This offers lower torque to gold prices. They already trade at much higher EV/oz valuations: A$2,400/oz and A$500/oz, respectively. Whereas ODY sits at only A$86/oz with a defined 407koz high grade resource still in the developer stage.

This gives ODY significantly more torque to a rising gold price and upcoming catalysts (scoping study, resource growth, production pathway), while New Murchison Gold and Meeka are already priced for their existing cash flow and have less explosive growth potential from here.

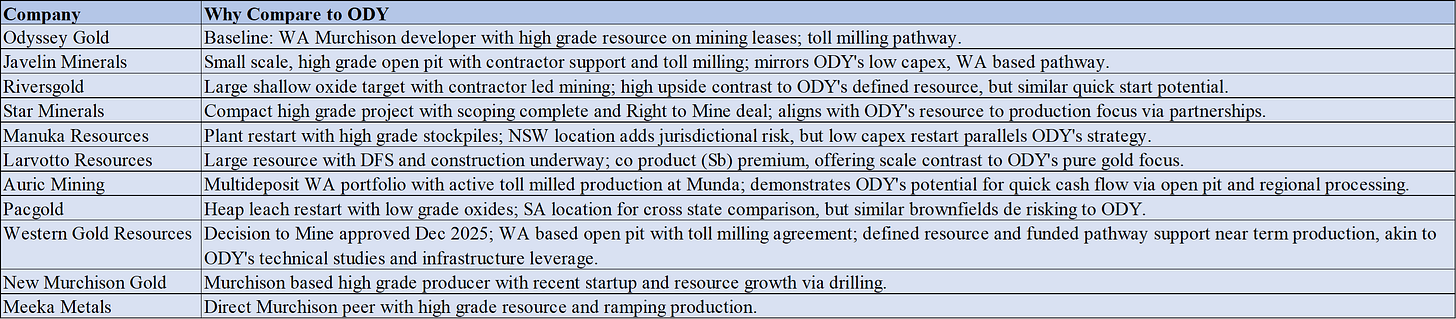

Reasons why peers are apt comparisons. Own research.

Conclusion

In summary, Odyssey Gold stands out as the cheapest near-term gold producer on the ASX, trading at a massive discount to its NPV (A$404M vs. A$49M market cap) with a funded, low-capex path to 2026-2027 production via toll mining.

While risks like execution delays or gold price volatility exist, the proven model, high insider/institutional ownership, and bullish gold outlook provide a substantial margin of safety. With ODY now over 5% of my portfolio, I see 200-300%+ upside potential, to catch up with peers. Upside is even larger if we assume it will reach NPV.

Even if I am wrong by a wide margin on my calculations, the discount to NPV is so large and the fundamentals so strong that I argue that it is worth a buy.

However, upside could be capped if another mining firms decided to buyout Odyssey at current stock prices or slightly above them.

Any feedback is more than welcome in the comments, or you can send me a message on Substack, or through my Twitter (X) account @AAGresearch.

As always, I want to thank my wife Yeimy, who has helped me a lot while I was writing this by myself. This report and this blog would not be possible without her. Thank you.

I hope this finds you well,

Alberto Álvarez González.

Disclaimer: I assume no liability for any and all of your actions, whether derived out of or in connection with this information or elsewhere, and you hereby warrant and represent that any and all actions that you take or that you may take at a later date in connection with this information shall remain your sole responsibility and, in case, I shall not be held liable for any such actions.

Link to report:https://aagresearch.substack.com/p/odyssey-gold-asx-ody-the-making-of?r=3hhq06