Summary

· On 2025, the equity investments I sold returned an average of 80%. Open equity investments returned an average of 172% in 2025.

· The sizing I had on Manolete meant that my returns were not as good, but it was a spectacular year for my portfolio, nonetheless.

· 2025 is the first full year I have run this blog. I started doing reports on the 29th of February 2024, so it was pointless doing a report on performance on January 2025.

Alberto’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Closed investments

My timing on the selling of AMRK and Ero Copper was bad in retrospect. With AMRK it was a bit outside my circle of competence, which was a mistake I made on the first place. With Ero Copper I blamed a lack of operational performance for the sale, but I should have bought a different copper stock.

Goliath Resources and Radius Gold are flat since I sold it, so I am happy with that decision.

Other stocks like Hannan Metals and Coppercorp are down 20% and 25% respectively since I sold them.

Aurion is up 100% since I sold it. But thankfully I kept Liberty Gold as my main gold play.

District Metals is up around 200% since I sold it. Which I find a bit odd since Sweden decided to legalize uranium mining. I think many of us believed that if the uranium mining ban was lifted the stock would be up 1000%. So, I am a bit disappointed on the stock, although of course I would have like to own it for a bit longer and enjoy the 200% ride upwards.

Regarding uranium my main regret this year was not investing in small modular reactor (SMR) stocks, which were clearly within my circle of competence. Now they are unfortunately overvalued.

Overall, I am happy with the decisions I made to sell in 2025. I was heavily invested in Boab and Goliath so that was good on my part.

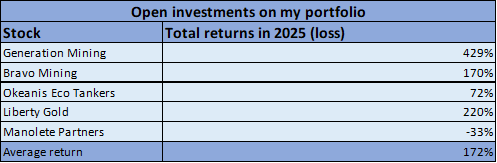

Open investments

2025 returns were mainly driven by higher platinum, palladium, gold and silver prices. You can find reports on all these metals on my blog. The only regret I have is not having invested more on these sectors.

Manolete Partners has obviously been a disappointment for now. The industry fundamentals are very strong, with insolvencies at all time highs, but management has not been able to rip the benefits from this tailwind.

Generation Mining has done an incredible job in 2025, they have obtained all the construction permits, expanded its land package by 36% and advanced financing. Generation now owns the most advanced pre-production PGM project in North America.

Bravo Mining remains my top pick for the PGM industry as Brazil offers a more streamlined permitting process than Canada, and management is a lot more invested in the business.

Bravo’s achievements in 2025 may require another report, but I will do my best to summarize it here: They have achieved the completion of a PEA, they have achieved access to an export processing zone and Bravo has also obtained their Preliminary License (LP) for the Luanga Project, the most time intensive permit in Brazil’s environmental licensing process.

At the beginning of 2026 Bravo announced that “Orion [Mine Finance Management] intends to commit to provide up to US$300 million of financing support by providing an indicative non-binding term sheet proposal in the form of equity, debt, and other financing instruments promptly upon notice of such milestones being met.”. This is a major milestone to obtain the necessary financing for the Luanga project.

Regarding the financing of the project, Generation Mining is more advanced than Bravo.

In 2025, Liberty Gold made significant strides in advancing its Black Pine Gold project in Idaho. The company achieved a key milestone in November with the receipt of a completeness determination from the U.S. Forest Service and Bureau of Land Management.

The company bolstered its financial position through a successful strategic 9.9% investment from Centerra Gold. Having a big mining firm on the shareholder registry is always a positive. Additional treasury support came from a US$2.2 million staged payment received in October related to the sale of its TV gold project interest.

However, the vast majority of the 220% return came from the 63% increase in gold prices. It was very nice that Liberty outperformed gold prices and the GDX gold miners ETF.

For Okeanis 2025 marked significant de risking through strong TCE earnings, successful capital raises for fleet modernization and growth. Plus, it was great to see consistent outperformance in a constructive tanker market driven by factors like aging fleets, low newbuild orders, and shifting oil trade flows. These efforts positioned Okeanis Eco Tankers for continued momentum into 2026.

Manolete has been extremely disappointing thus far. In the half year period ended 30 September 2025 (H1 FY26), results showed revenue of £12.7 million (down 12% from the prior comparable period). This reflects variability in realized case values and some one-off impacts, but the company maintained a solid pipeline of new cases and emphasized its resilient business model focused on high quality insolvency claims.

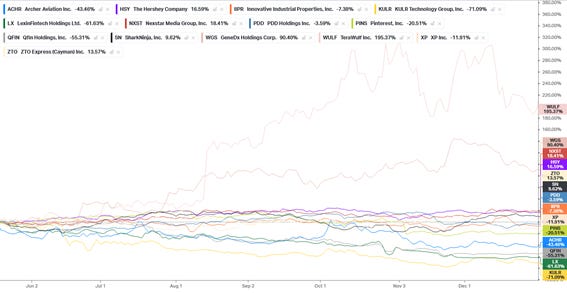

Open put options

These have been the 2025 returns of the stocks I bought put options of in May 2025. Eight have these stocks have had a negative return (positive for my put options), and I am happy with the performance thus far. Those options that were about to expire have been rolled forward into late 2026. Remember this portfolio of options “only” make up just under 10% of my total portfolio.

Any feedback is more than welcome in the comments, or you can send me a message on Substack, or through my Twitter (X) account @AAGresearch.

As always, I want to thank my wife Yeimy, who has helped me a lot while I was writing this by myself. This report and this blog would not be possible without her. Thank you.

I hope this finds you well,

Alberto Álvarez González.

Disclaimer: I assume no liability for any and all of your actions, whether derived out of or in connection with this information or elsewhere, and you hereby warrant and represent that any and all actions that you take or that you may take at a later date in connection with this information shall remain your sole responsibility and, in case, I shall not be held liable for any such actions.

Alberto’s Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Link to report: https://aagresearch.substack.com/p/2025-portfolio-review-good-returns?r=3hhq06