By James Kwantes

Published first at Patreon

Mining companies are printing plenty of money at these metals prices. That makes the depletion of their reserves, week by week and year by year, even more of a pressing issue.

Excitement is building - PDAC hit a record attendance of 32,155 people - and we're at that point in the metals cycle where cash-rich mining companies begin or accelerate deploying their treasuries to replace those reserves.

We know this because the guy in charge of the world's best-run gold mining company, Agnico Eagle (AEM-T), recently said it out loud.

During the company's Feb. 13 earnings call, Agnico CEO Ammar Al-Joundi said the world's No. 2 gold miner by market cap is "very well-positioned" to pursue accretive acquisitions, with the "strongest balance sheet in our history." Agnico reported record annual free cash flow of $4.4 billion last year and net cash of $2.67 billion, following 2025 production of 3.45 million ounces.

"We are willing to move - and we have moved - when we see an opportunity on the M&A side that actually creates value per share," he said.

Quite a shift from September, when gold traded between US$3,500 and $3,800. At the time, Al-Joundi warned about "irresponsible M&A" driven by the surging gold price.

'EXPLORATION UPSIDE' KEY

Al-Joundi told investors and analysts on the call that strong exploration potential was a key to identifying the best opportunities: "What would really interest us - and what has really driven us for external M&A - has really been exploration upside."

Two gold camps where Agnico already has a strong presence came to mind immediately: Finland's Central Lapland Greenstone Belt and Canada's Yukon.

Central Lapland Greenstone Belt (CLGB) of Finland

Finland won bronze in Olympic men's hockey, but there's gold in the country's future. Probably lots of it.

The CLGB is an emerging gold district with geological similarities to other prolific greenstone belts such as the Abitibi (85M oz total production) in Canada and the Zimbabwe Craton (40M oz). Yet the belt hosts just one producing gold mine: Agnico Eagle's Kittila mine. Kittila, Europe's largest gold mine, produced 217,379 ounces of gold in 2025. That's about 6.3% of Agnico's production. About nine million ounces of gold have been mined so far.

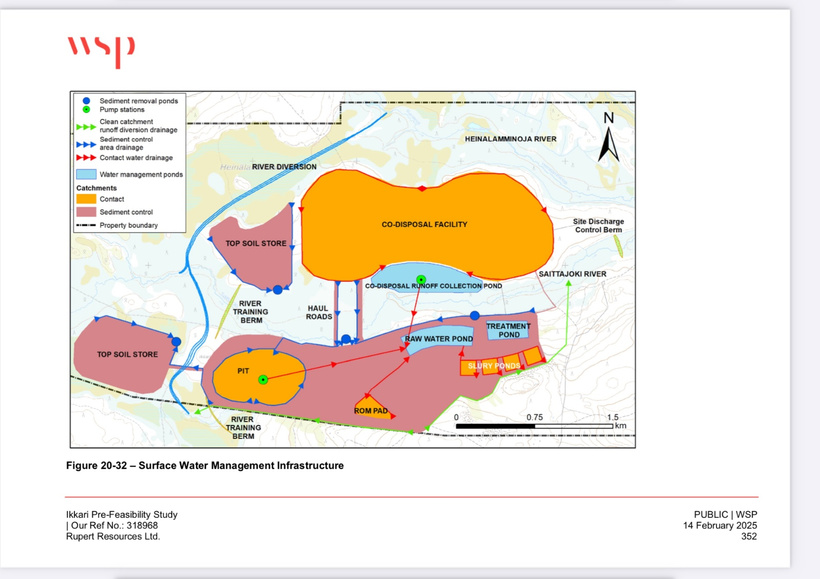

The CLGB also hosts one of the world's most promising gold discoveries in recent years: Rupert Resources (RUP-T)'s Ikkari deposit. In 2021, Rupert reported a maiden resource estimate of 3.95 million ounces based on just 36,000 metres of drilling. A prefeasibility study released in 2025 reported 3.5M oz in proven and probable reserves, at 2.1 g/t Au, and showed an NPV (5% discount) of $1.7 billion at US$2,150 gold. Agnico Eagle owns a 13.9% stake in Rupert.

On Feb. 19, Rupert announced Ausenco would lead the feasibility study for the Ikkari deposit. There's a fly in the ointment, however, and it's either a positive or a negative depending on your perspective.

BOUNDARY ISSUES

Gold deposits don't answer to property boundaries, and the Ikkari deposit is right beside JV ground held by Aurion Resources (AU-V) (30%) and B2Gold (BTO-T). It's also very close to Aurion's 100% owned ground. There's a pretzel flavour to Rupert's economic studies, as the company twists and turns to tailor everything from the Ikkari pit shape to location of the waste dumps to a river diversion (!).

Resolving this issue would materially strengthen Ikkari economics.

In addition to the infrastructure issue, gold mineralization at Ikkari extends onto the Aurion-B2Gold JV ground - as much as 600,000 ounces, according to B2Gold CEO Clive Johnson in a 2024 B2Gold conference call.

Hits at Helmi, on the JV side of the boundary, include 2.05 g/t Au over 77.5 metres and 2.44 g/t over 43.45m.

So far, Rupert has been unable to get a deal done with Aurion (and JV partner B2Gold), despite attempts. Two years ago, Rupert offered B2Gold $102.8 million worth of Rupert shares for its 70% interest in the JV, implying a $44M valuation for Aurion's 30% (at US$2,000 gold). Aurion has a right-of-first-refusal on B2Gold's 70%, which it elected not to exercise at the time. The Rupert-B2Gold deal fell through.

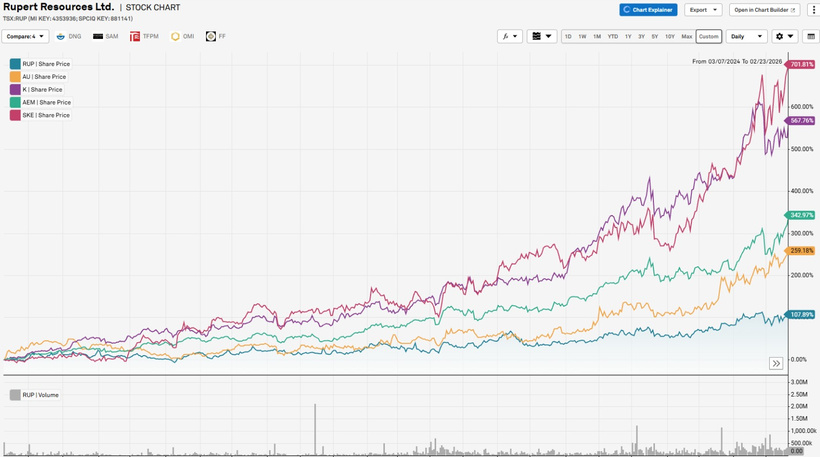

In the intervening two years, gold has surged and so have shares of most of the miners and developers. Skeena stock has rocketed 700% higher, Kinross is up 568% and Agnico Eagle has risen about 340% in that time frame. Aurion shares are up about 260%. Rupert shares have lagged (they've risen 108%), which could make getting any stock deal problematic - or a lot more expensive.

Intriguingly, in August 2025 Aurion announced a new, anonymous strategic investor who bought a $9.29-million unit offering, giving them 6.88% of Aurion shares and 9.98% on a partially diluted basis. Could the anonymous investor be Agnico Eagle? Stay tuned.

Aurion is a major exploration player in the CLGB, with gold discoveries on both its 100% owned Risti property and on its 30% owned ground held in the JV with B2Gold. Kinross owns 9.7%; Aurion chairman Dave Lotan more than 9.8%. Aurion has option deals with Kinross (Launi East) and KoBold Metals, a private critical minerals exploreco backed by Jeff Bezos and Bill Gates.

Another exploreco active in the belt is Firefox Gold (FFOX-V), which is exploring its Mustajarvi discovery in the eastern CLGB. Mustajarvi is part of the Sirkka Shear Zone, an important fault system that hosts Ikkari, Helmi and other gold discoveries. Agnico Eagle owns 11% of Firefox and is earning in to a large prospective land package.

Consolidation makes a lot of sense in this belt and Agnico Eagle is the logical consolidator, as Rupert's largest shareholder and operator of the nearby Kittila gold mine.

Rupert Resources (RUP-T)

Price: $7.86

Shares out: 235.4 million

Market cap: $1.85 billion

Aurion Resources (AU-V)

Price: $1.84

Shares out: 162.5 million (179.5M fully diluted)

Market cap: $299 million

Yukon's Tintina Gold Belt in Canada

Canada's Yukon needs no introduction as a prolific gold belt, one that's enjoying a resurgence fuelled by discoveries and the bull market.

The hottest discovery story is Snowline Gold (SGD-T), which has rocketed from dimes to $19 in the past five years as gold mineralization grows both within and outside the proposed Valley open pit. Once Snowline is taken over and the mine built, Valley will be a major driver of the Yukon economy and one of Canada's largest gold mines.

The ounces are building in Yukon, with Sitka Gold (SIG-V) the latest to publish an updated resource at its RC project. Current tallies (some of the grades are blended):

Snowline Gold: 7.94M oz (M&I), 1.21 g/t Au

Banyan Gold: 7.6M oz (I&I), 0.61 g/t Au

Sitka Gold: 5.12M oz (I&I), 0.83 g/t Au

White Gold: 3M oz (I&I), 1.4 g/t Au

Fuerte Metals: 3.8M oz (MI&I), 1.24 g/t Au

That's more than 27 million ounces of gold, in relatively close proximity and in a mining-friendly jurisdiction. It's a state of affairs that is unlikely to continue, especially in this kind of gold market. Consolidation makes a lot of sense.

Add in Western Copper and Gold's low-grade but enormous gold endowment (21.1M oz (MI&I), 0.17 g/t Au), and Yukon clearly qualifies as a world-class mining camp. Several majors are already positioned, including Agnico Eagle.

GOLDEN EAGLES

A wild card is the sale of Yukon's Eagle gold mine formerly operated by Victoria Gold, which went bankrupt following a 2024 heap leach failure that closed the mine. Restoration and safety work continues at the site and a large safety berm has been constructed.

Eagle has reported resources of 4.7 million ounces including 3.3M oz of reserves (at 0.65 g/t). Receiver PricewaterhouseCoopers (PwC) is running an auction process for the mine and there are apparently three final bidders. One of them could well be Agnico Eagle.

Franco-Nevada recently spent $52.5 million to buy a 6% NSR on Banyan Gold's AurMac property from PwC. The NSR was previously held by Victoria Gold; 1% can be bought down for $10 million.

Agnico Eagle already has a Yukon presence. Agnico is a long-standing shareholder of White Gold (WGO-V), owning 19% of the company. Agnico also owns 8% of Tim Warman's Fuerte Metals (FMT-V), which is developing the Coffee gold mine discovered by Rob Carpenter's Kaminak Gold.

On the exploration front, Carpenter's latest play, Prospector Metals (PPP-V), landed on the radar in Yukon last year with gold discoveries including 44 metres of 13.79 g/t gold, 38.08 g/t silver and 1.84% copper (announced Oct. 1, 2025) at its ML project northeast of Dawson City. About 25,000 metres of followup drilling is planned this year.

The $82-million Yukon drill hole | Oct. 2, 2025

One possible scenario is a major swooping in to purchase both the Eagle gold mine and Snowline Gold. Such a move could provide both immediate cash flow from Eagle as well as decades of production runway at Snowline's Valley, which will take several years to get permitted and built. Snowline has vast claims holdings that are highly prospective for future discoveries.

Agnico Eagle has Northern operating experience, a strong balance sheet, a market cap of $173 billion and a strong currency in the form of an elevated share price. Seems like a good potential fit.

Snowline Gold (SGD-T)

Price: $18.75

Shares out: 173.7 million (185M fully diluted)

Market cap: $3.26 billion

Prospector Metals (PPP-V)

Price: $1.40

Shares out: 155.35 million (177.3M fully diluted)

Market cap: $217.5 million

Disclosure: I own shares of Aurion Resources, Snowline Gold and Prospector Metals, and am doing communications consulting with Prospector. No business relationship with any other company mentioned. This article is for informational purposes only and all investors need to do their own due diligence.